Or how the system we consider “normal” today came to be

Throughout history, one recurring theme appears: the effort of a small, narrow group of people to control the monetary system. This is not a matter of decades, but centuries.

For at least the past 300 years, in different historical periods, the same goal can be observed—one central bank, one global currency, and eventually, one world government.

When someone starts to truly study the history of money and banking, it becomes clear that these are not random events. On the contrary, it is a step-by-step process carried out very systematically.

Central Banks as Tools of Power

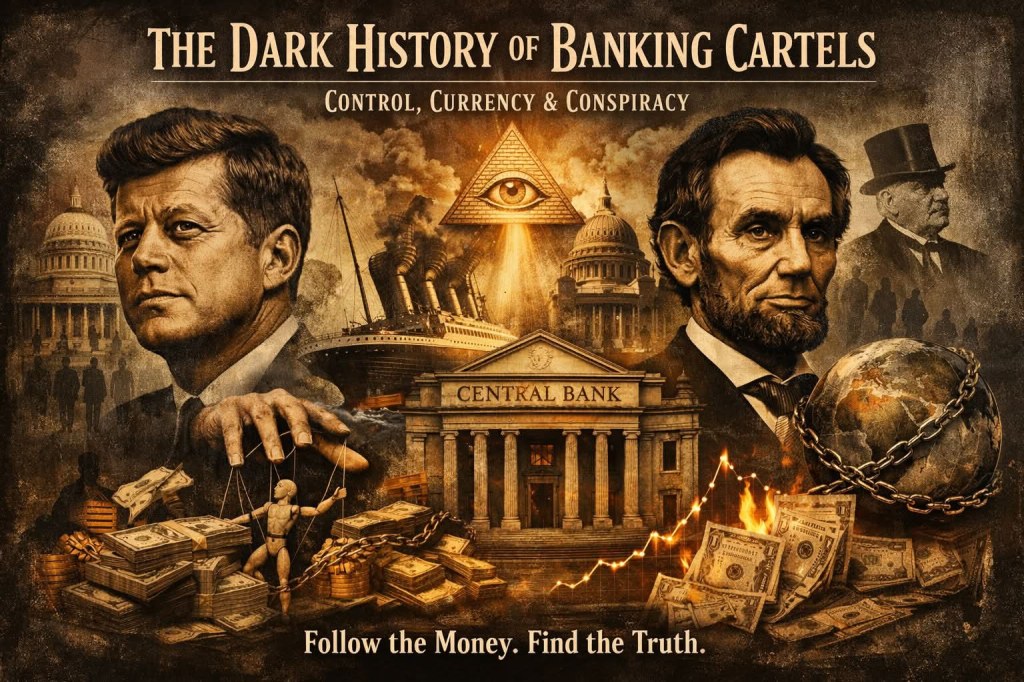

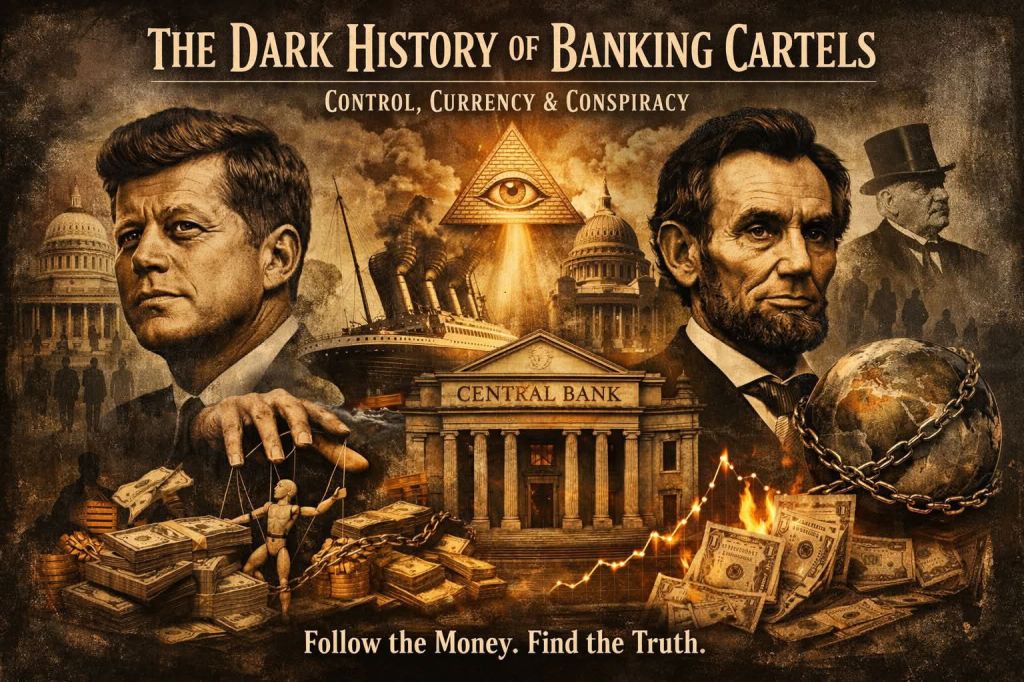

A typical modern example is the U.S. Federal Reserve System (the Fed). Its creation involved well-known names and powerful families that are rarely discussed today. However, it is not entirely true that the Fed was the first or the most decisive milestone.

Historical sources suggest that the real turning point was the establishment of the Bank of England at the end of the 17th century. This central bank was private—and it became the model for other central banks around the world. Although today names like “central bank” or “national bank” sound very state-related, the reality is often quite different.

Interestingly, the establishment of central banks coincided with massive taxation of the population. Taxes, which were practically unknown to civilizations before, became the norm. The first income tax appeared shortly after the Bank of England was founded. Coincidence?

Resistance and “Coincidences” in History

History also shows that there was strong opposition to this system. Influential figures, politicians, and entire groups of people understood how dangerous private control of currency could be.

Abraham Lincoln opposed central banking. John F. Kennedy attempted to return the right to issue money to the government. We all know how they ended. Similarly, people who resisted the creation of the Fed perished on the Titanic, while its supporters decided at the last minute not to board.

These may be coincidences—but there are far too many “coincidences” in history to ignore.

Money from Nothing and the Theft of Energy

Today’s fiat currency system operates on a simple principle: money is created from nothing. Since 1971, it is no longer backed by gold or any tangible value. Yet we use it to buy real goods, labor, and energy.

Inflation is now considered normal. Central banks openly state that their goal is 2–3% inflation per year. In other words—they take a portion of the value of our work every year and call it proper system functioning.

Money is essentially stored energy and time. When someone causes inflation, they are stealing your energy. They are stealing your life’s time.

Debt-Free Money and Forgotten History

History shows that debt-free money has existed. In the early days of the United States, the system worked without a central bank, without interest, and without inflation. The government issued money directly, without creating debt—and it functioned.

But once central banks entered the picture, state and citizen indebtedness followed, creating an endless cycle of interest that must be repaid through ever-increasing taxes.

It is no coincidence that Thomas Jefferson warned that banking institutions are more dangerous than entire armies. And Henry Ford aptly remarked that if people truly understood the banking system, there would be a revolution tomorrow morning.

In Conclusion

This is not about conspiracy theories, but historical facts, quotes, and connections that anyone can verify. The problem is not that this information doesn’t exist—the problem is that most people never take the time to explore it.

Those who understand the system often profit from it, and therefore have little incentive to change it.

The question remains: how long can this system be sustained—and at what cost in energy, time, and freedom?

Leave a comment